Customer churn is the silent drain on growth that every subscription fintech watches closely. Over the years I’ve worked with startups and scale-ups in payments, neobanking, and crypto wallets, I’ve noticed that churn rarely arrives without warning. It whispers first — in small behavioral shifts — and those whispers become predictable if you know what to listen for.

In this article I’ll share the three data signals I rely on to predict early churn in subscription fintechs. These are not abstract theories; they’re practical, measurable signals I’ve validated across cohorts and product models. I’ll explain what to track, how to interpret each signal, and the practical interventions that can reverse the trend.

Engagement decay: the gradual drop in core product usage

Engagement is the heartbeat of any subscription product. For fintechs, "core usage" might mean daily active sessions, transaction frequency, card swipes, bill payments, or logins to view portfolio updates. When that heartbeat slows, churn risk rises.

I look at two sub-metrics within engagement:

What makes this signal powerful is that it appears early — often weeks before cancellation. A user who previously logged in five times a week and drops to once per week has lost daily context and habit. For fintech products that rely on habit (think budgeting apps or micro-investing platforms like Acorns), habit decay is a leading indicator of churn.

How I monitor it:

Actions that work:

Support signal anomalies: rising friction and unresolved issues

Support interactions are an exceptional early warning system. When the volume or tone of requests shifts — especially around billing, account access, or perceived value — customers start thinking about leaving. I don’t just look at volume; I analyze sentiment, resolution time, and recurrence.

Key sub-metrics I track:

Real examples I've seen include new fee structures causing confusion, card declines tied to KYC issues, or failed payouts in small-business payroll products. These incidents create a pronounced churn spike if not addressed quickly.

Implementation tips:

Monetary engagement changes: drop in transaction value or frequency

For subscription fintechs, money movement is often the clearest expression of customer commitment. A user who stops transacting, reduces wallet balances, or decreases recurring deposit amounts is signaling decreased attachment. I separate monetary signals from general engagement because they often indicate a concrete shift in financial behavior.

Monetary metrics I use:

These signals are particularly predictive when combined with engagement decay. For example, a user who logs in less and transfers less money is far more likely to churn than a user who only has one of those behaviors.

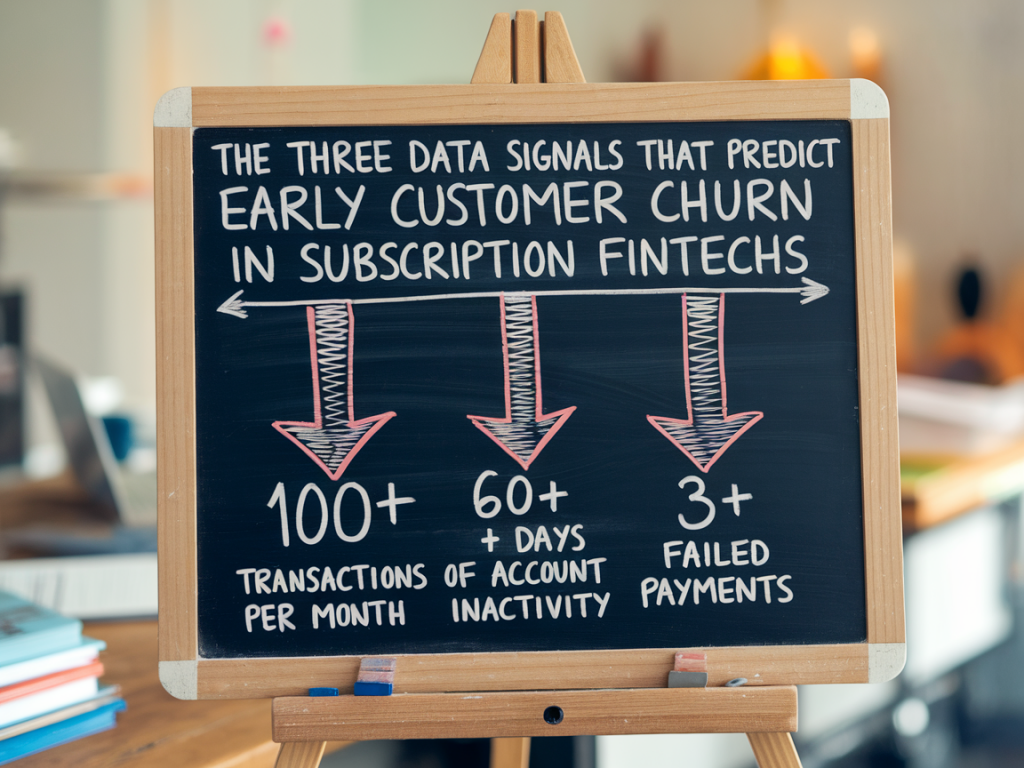

Practical thresholds I’ve used:

Interventions that work:

Putting the three signals together: a simple health-score matrix

None of these signals is perfect in isolation. The most effective approach is to combine them into a composite health score that weights each signal by predictive power for your specific product. Below is a sample table I use as a starting point — adjust weights and thresholds based on historical churn analysis.

| Metric | Why predictive | Typical action |

|---|---|---|

| Engagement decay | Loss of habit reduces perceived value | Re-engage with personalized nudges and frictionless in-app actions |

| Support anomalies | Unresolved friction leads to dissatisfaction | Fast-track resolution, human outreach for high CLV |

| Monetary changes | Concrete reduction in financial commitment | Incentives, value recaps, product education |

When two or more signals light up within a short window (7–30 days), I treat the user as high-risk and trigger an escalation workflow. Low-risk users may get automated nudges; high-risk users get bespoke interventions.

Practical tips for implementation

If there’s one truth I’ve learned, it’s that churn is not binary — it’s a process. By listening to engagement, support, and monetary signals together, you can catch customers long before they cancel and design interventions that feel helpful rather than intrusive. The data speaks; it’s our job to hear it and act quickly.